The Internal Revenue Service (IRS) periodically reviews employers’ tax liabilities to determine appropriate federal tax deposit schedules. Recently, the IRS has been issuing Notice CP136 to inform employers of changes to their deposit requirements for Form 941, the Employer’s Quarterly Federal Tax Return. Understanding this notice is essential for maintaining compliance and avoiding potential penalties.

What is Notice CP136?

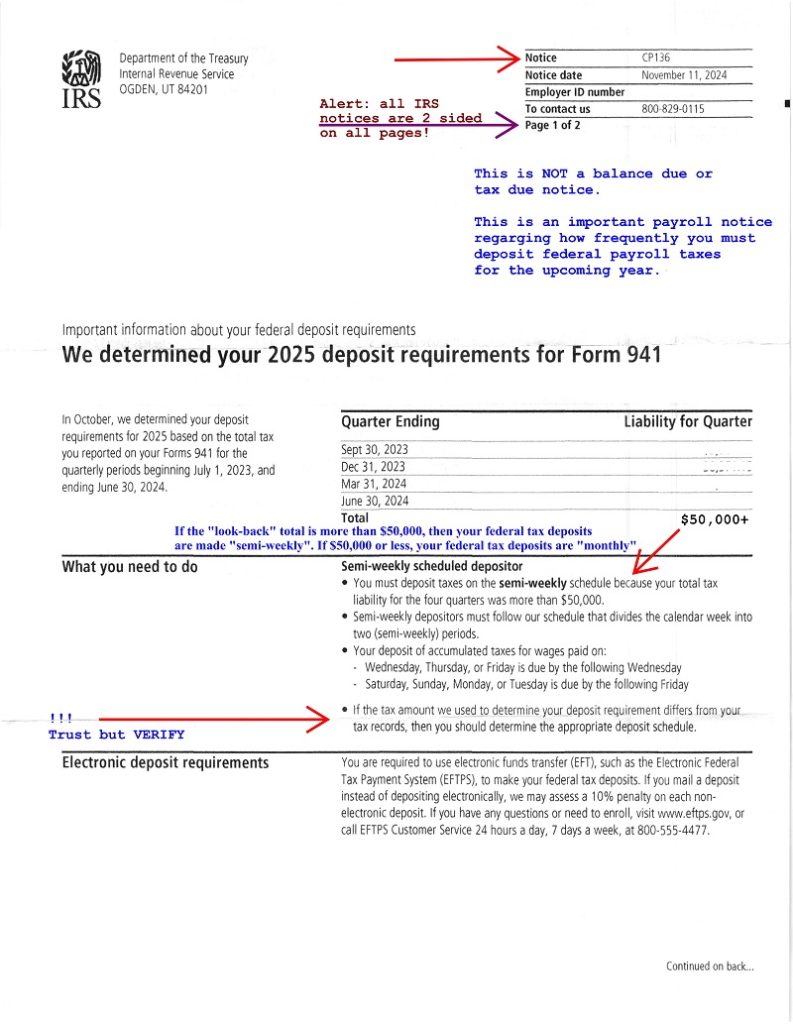

Notice CP136 is an official communication from the IRS notifying employers of a change in their federal tax deposit schedule for the upcoming year. This change is based on the employer’s total tax liability during the “lookback period,” which consists of the four consecutive quarters ending on June 30 of the previous year. Depending on the total tax reported during this period, an employer’s deposit schedule may change from monthly to semi-weekly, or vice versa.

Deposit Schedules Explained:

- Monthly Depositors: Employers with a total tax liability of $50,000 or less during the lookback period are classified as monthly depositors. They must deposit taxes on wages paid during the month by the 15th of the following month.

- Semi-Weekly Depositors: Employers with a total tax liability exceeding $50,000 are classified as semi-weekly depositors. For wages paid on Saturday, Sunday, Monday, or Tuesday, taxes are due by the following Friday. For wages paid on Wednesday, Thursday, or Friday, taxes are due by the following Wednesday.

Key Actions for Employers:

Communicate with Payroll Providers: If you utilize a payroll service, inform them of the change so they can adjust your deposit schedule accordingly.

Review the Notice: Carefully read Notice CP136 to understand your new deposit schedule.

Verify Accuracy: Compare the tax amounts listed in the notice with your records. If discrepancies exist, determine the appropriate deposit schedule based on your records.

Update Payroll Processes: Adjust your payroll systems to comply with the new deposit schedule starting January 1 of the upcoming year.

Electronic Deposits: Ensure all federal tax deposits are made electronically, as required by the IRS. Exceptions apply if your tax liability is less than $2,500 for the quarter.

Additional Considerations:

- $100,000 Next-Day Deposit Rule:

If your accumulated tax liability reaches $100,000 or more on any day during a deposit period, you are required to deposit the tax by the next business day, regardless of your regular deposit schedule. This rule applies to all employers, irrespective of whether they are monthly or semi-weekly depositors. - Penalties for Late Deposits:

Failing to adhere to the correct deposit schedule can result in penalties. The penalty amount varies depending on how late the deposit is and the total amount due. Ensuring timely deposits is crucial to avoid unnecessary costs.

Steps to Ensure Compliance:

- Set Up Alerts:

Use your accounting or payroll software to set reminders for your new deposit schedule. Staying ahead of deadlines will reduce the risk of errors or missed deposits. - Monitor Your Tax Liabilities:

Regularly review your payroll tax liabilities to ensure your deposits are accurate and align with IRS expectations. This is especially important if your business experiences growth or changes that could impact your tax responsibilities. - Consult a Tax Professional:

If you’re uncertain about the details in Notice CP136 or how to implement the changes, consult with a tax advisor. Professional guidance can help you stay compliant while optimizing your processes.