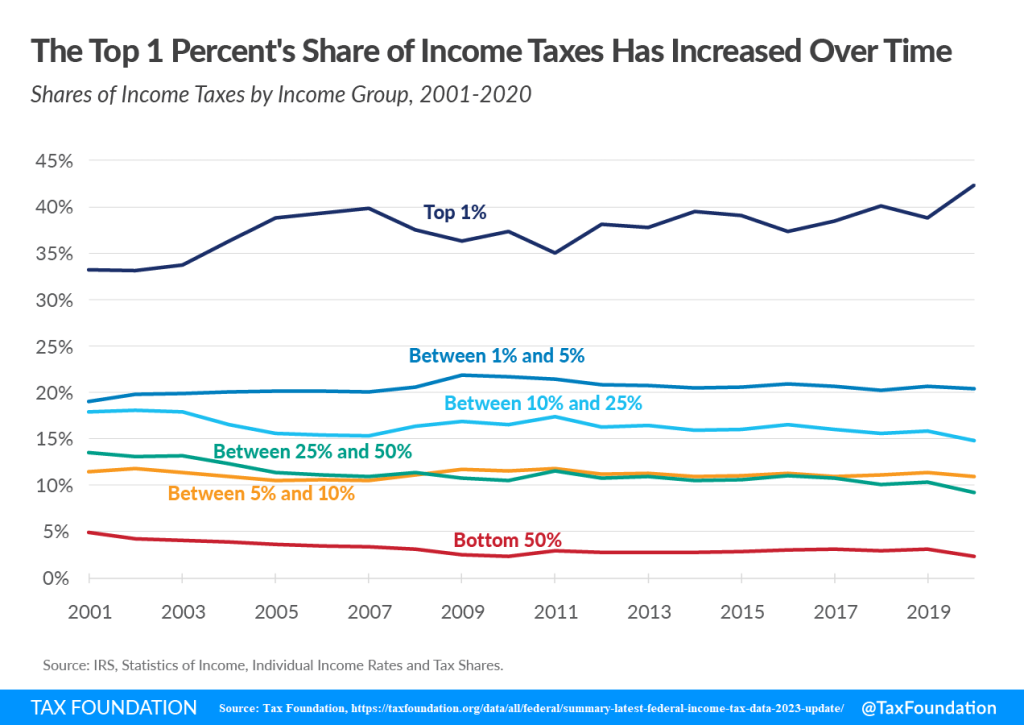

Why did Willie Sutton famously say he robbed banks? “Because that’s where the money is!” So why, then, don’t we tax the rich? Well, we do! The bottom 20% of American earners, who make less than $30,000, contribute less than 1% of the total tax bill. The top 20%, earning over $190,000, pay 67% of all individual income taxes collected. That amounts to roughly 25% of their income. And the top 1%, earning over $982,600, pay a whopping 26% of all income tax collected. That amounts to 31% of their income.

And still, last year, Uncle Sam spent $1.7 trillion more than he took in. Way to go, Washington!

Naturally, government offices and DC think tanks are full of clever people looking for ways to wring more tax dollars out of all of us without crimping the economy that generates all that income in the first place. And it’s not escaped their attention that some of the very wealthiest have found a way around that average 31% bite. Specifically, those who own stock in publicly traded companies can choose not to sell it, which would generate taxable capital gains. Instead, they can monetize it in the form of tax-free loan proceeds. It’s called the “buy, borrow, die” strategy.

In 2021, an IRS contractor named Charles Littlejohn leaked a trove of tax data, including 15 years of data from thousands of the wealthiest Americans. (Last month, a federal judge sentenced him to five years in jail for the unlawful disclosure.) His leak revealed just how much those millionaires and billionaires can spend on mansions, yachts, and jets without spending a dime on taxes. Take Elon Musk, for example. In 2015, Tesla sold 50,658 shiny all-electric cars. Musk paid $68,000 in federal income tax. In 2017, he paid $65,000, and in 2018, nothing at all.

Several senators have proposed a new wealth tax on net worth above $50 million. However, their approach would require those taxpayers to appraise and report every asset they own on an annual basis, which would make it fatally hard to administer and enforce. Last month, two professors from the University of Michigan and Yale law schools published a paper taking a simpler approach. Their 15-page proposal, packed with 70 detailed footnotes, takes dead aim at the “buy, borrow, die” approach to raise $100 billion over the next 10 years.

Their analysis used Oracle founder Larry Ellison as its avatar. Ellison is currently the fifth-richest man on the planet, worth $140 billion. He’s used his vast fortune to pick up an impressive collection of grown-up toys: two America’s Cup sailing victories, a $270 million yacht, and 98% of Hawaii’s sixth-largest island. Yet he hasn’t sold his stock to do it. Instead, records show, he’s pledged $30 billion of his Oracle stock to secure “personal indebtedness. (Extra bonus break: when Ellison dies, the outstanding debt will reduce his eventual estate tax!)

Their solution: a “billionaire borrowing tax” that would tax Ellison as if he had actually sold that stock when he uses it to secure a loan. The tax would kick in for families with “major assets” (business interests and land) worth $100 million or above. And there’s plenty of fine print, of course, in the form of a $1 million lifetime exemption, $200,000 annual exclusions, and detailed rules for calculating the taxable amount and stepping up the basis in the encumbered stock on future sales.

You may not think you need to worry about a “billionaire borrowing tax.” But it’s a sign of a very real threat. The government needs more money, and they have to find it somewhere. Proper planning is how to keep them from looking for it in your pocket, whether you’re a billionaire or not!